💡 STANDARD DEVIATION & BETA 💡

In simple terms, the risk is the probability of loss or uncertainty of outcome. What does it mean if you are investing in the equity market? Here, the return on equity investment is uncertain, and that uncertainty is known as risk. In the context of equity investments, risk can be classified into two parts: systematic risk and unsystematic risk.

Systematic risk:

Also known as market risk, this is measured through an indicator known as beta. Systematic risk affects the overall market. It is neither sector-specific nor related to any specific company. However, it may have different impacts on various sectors and companies. Interest rates, inflation, and economic and political risk are examples of systematic risk. These risks cannot be reduced by diversification. This is why systematic risk also goes by another name: non-diversifiable risk.

Unsystematic risk:

This is a company- or sector-specific risk. That means it has impacts on only particular companies or sectors. Credit risk, management risk, and operational risk are examples of unsystematic risk. These risks can be reduced with the help of diversification. This is why systematic risk is also referred to as diversifiable risk.

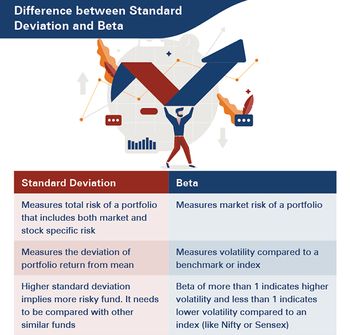

STANDARD DEVIATION

Standard deviation is used to measure the total risk of a portfolio. Total risk is the sum of systematic risk and unsystematic risk. Here’s a simple formula:

Total Risk = Systematic Risk + Unsystematic Risk

(This is expressed as a percentage figure that is annualized.) Aside from being an indicator of a portfolio’s overall risk, standard deviation also reveals the consistency of the returns. It can be measured by calculating the deviation from the mean.

High standard deviation: This suggests that the fund experiences high volatility and is therefore subject to high risk.

Low standard deviation: This generally implies consistency in the fund’s performance and suggests that the fund is a low-risk one.

BETA

Beta measures the volatility of a stock or fund with respect to stock indices like Nifty whose beta is considered as one.

Let’s consider two possibilities:

• A fund’s beta is more than one: Such a fund is considered more volatile than its index. It is preferred by aggressive investors who have high-risk appetites.

• A fund’s beta is less than one: Such a fund experiences low volatility. It is suitable for conservative investors who have a low tolerance for risk.

Beta also represents the market risk or systematic risk. The beta of a fund is the weighted average of individual stocks in a fund.