Two reasons why it is becoming increasingly challenging to trade non-directional option strategies

1. Premiums:

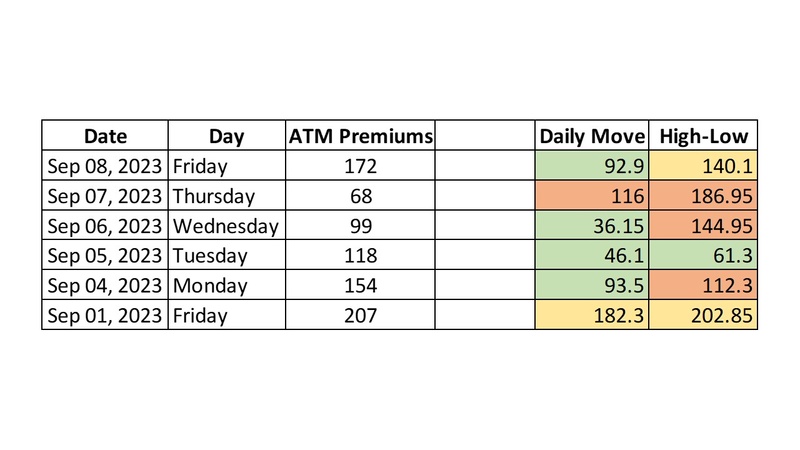

Based on observations made on September 1, 2023, it was noted that the At-The-Money (ATM) premiums were pricing in 207 points for the entire week (5 days). On the same day, the markets moved by 202 points.

Similarly, it can be observed that on 3 out of 6 days, the market moved nearly the same number of points as the short straddle premiums were pricing for the entire week.

This figure is notably high, as 50% of the time, the risk pricing for the entire week is being breached in a single day. This is just one of the factors.

2. IV Spikes:

The other factor to consider is the occurrence of IV (Implied Volatility) spikes. In the previous week, an average of two significant IV spikes were witnessed each day.

When the market moves in a certain direction, the premiums of one leg increase while the counter leg doesn't decrease, resulting in substantial Mark-to-Market (MTM) losses despite having a correct directional bias. Out-of-The-Money (OTM) options are surging by as much as 2-3 times their value in a very short time span.

Solution:

These two factors are forcing sellers to constantly shift or adjust their positions. Due to the low premiums, even the risk-to-reward ratio is not favorable.

One bad trading day where you are caught in the wrong direction may take 2-3 weeks to recover from it.

In such times, more than striving for substantial profits, it tests your ability to manage risk and prevent giving back all your gains to the market. (Staying at the crease and not losing your wicket matters more than scoring runs.)

Effective risk management is key during these periods.

One idea to approach is to calculate the average profit you've made on your profitable days in the past two weeks and ensure that your losses do not exceed that amount.