Axis Bank Q4: NPA issues decisively behind, margin and RoE improvement eyed

Axis Bank (CMP: Rs 780; Market cap: Rs 239,455 crore) had a healthy quarter, with asset quality improving, loan growth ramping up in its target area, and deposit profile maintaining constant. Although the cost increase is a short-term disadvantage, it should provide the necessary competitive advantage in terms of technical competence. With asset quality problems substantially resolved, the emphasis should progressively improve profitability - raising its interest margin, which is now behind peers, and gradually increasing the RoE (return on equity) to the 18 percent objective. Given the stock's outperformance over the last three months, it may consolidate in the short term. However, we remain optimistic for the long run on two fronts: an improved earnings outlook and the likelihood of a valuation gap shrinking with peers as return ratios improve.

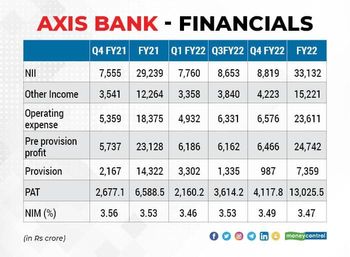

Despite strengthening its balance sheet with a more robust provision cover, the bank's profitability increased in FY22 primarily due to improved asset quality, which resulted in a minor provision. With a generally consistent margin, loan growth exceeded the sector.

ASSET QUALITY

The asset quality picture has continued to improve, sequentially decreasing non-performing asset slippage. There was a significant improvement and a healthy comeback from accounts that had been written off. As a consequence, reported gross and net NPLs improved sequentially. In addition, the provision coverage ratio increased sequentially from 72 percent to 75 percent.

Despite the provisioning increase, annualized gross and net credit costs fell sequentially to 71 and 32 basis points, respectively, and fell below the bank's long-term average for the third quarter in a row.

GROWTH STARTED PICKING UP IN THE FOCUSED SEGMENT

Axis Bank finished FY22 with a 15 percent increase in advances, far ahead of the industry average. However, because of significant price pressure, it avoided corporate lending and concentrated on SME and retail loans.

MARGIN WOES- KEY CHALLENGE OR THE PRINCIPAL OPPORTUNITY

Axis Bank's interest margin fell four basis points sequentially in Q4 to 3.49 percent, owing to an interesting reversal of Rs 83 crore. However, to enhance its total profitability and return ratios, the bank must make significant improvements to its interest margin.

The bank has close to Rs 96,190 crore in surplus liquidity, which, should it diminish with the resumption of growth, will have a beneficial influence on the interest margin. The steady improvement in deposit quality, a higher share of rupee lending versus overseas dollar lending, an increase in the share of high-yield lending such as unsecured retail that the bank feels confident about given its provision buffer, and a decline in the share of RIDF (Rural Infrastructure Development Fund bonds) with a negative spread should all help margin.

While the sharp increase in operating expenses has pushed the cost to assets ratio well above the target of 2%, management is not in a hurry to lower it to the coveted target of 2% because it believes that investment at this stage is critical for the technology-driven transformation journey to be future-ready. This should not be a problem if the bank improves its margin management.

The bank is well capitalized (capital adequacy ratio of 18.54 percent, CET 1 ratio of 15.25 percent) and optimistically targets profitable expansion by FY25, with an 18 percent return on equity objective. Axis Mutual Fund, Axis Capital, and Axis Securities are among the company's subsidiaries that are gaining pace. The company trades at a discount to its main private-sector rivals at 1.8X FY23e book value. Only a significant increase in margin, improved return ratios, and a low credit cost can minimize the value difference. Nonetheless, we feel that Axis Bank is a long-term winner and that every pullback is a chance to purchase.

#AXISBANK #QUARTERRESULTS