The NFO Wave - Successor For The IPO Wave

In an economy, where low interest rates and easy access to cash have fueled an iconic bull run and a never-seen-before IPO frenzy, we have yet another implication of the unduly high liquidity in the Indian Money Market – The NFO Wave.

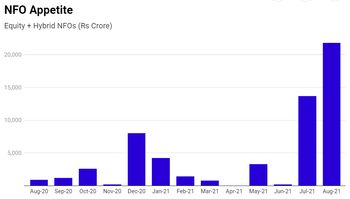

INR 22,720 crores – This is the amount that five newly launched equity schemes were able to raise in inflows in the month of August 2021, the highest ever ion magnitude since the SEBI reclassification of Mutual Fund Schemes. Along similar lines, a “Balanced Advantage Fund” by SBI had raised INR 14550 crores, again the highest inflow in NFO since this reclassification. The second-highest inflow stands at ICICI Pru Flexi-cap Fund’s NFO at INR 9800 crores, debuted in the month before.

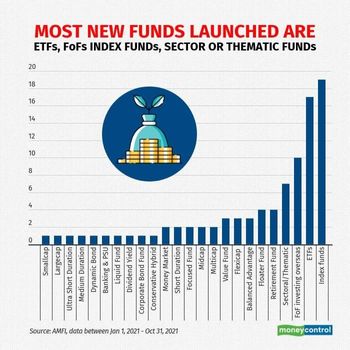

These inflows stand at stark contrast of movement observed over the course of the last year in the pooled asset management industry, which was marked with redemptions & outflows of INR 42200 crores, particularly from equity schemes amidst rallying indices. We can also argue that this new wave of NFOs has been a move on the part of AMCs to offset redemptions and maintain their status quo as the INR 30-trillion-and-frowing industry it is. Having collected over INR 76,000 crores this FY with an average of 10 NFOs, every month this race has been dominated by introduction of passive-index function, ETFs and Overseas Funds.

However, institutional investors hold the belief that a combination of excess-liquidity aided by a major bull-run in the global equity markets has been the driving force for this NFO wave. An interesting and strongly palatable argument rests on the line that the recent IPO listing premiums have prompted expectations of similar caliber from NFOs. A misguided notion that the listing NAV of INR 10 is too cheap to not put your hat in the ring, further aggravated by the Fear-of-Missing-Out driven by friends & family making bumper listing gains.

• From the supplier’s side we can understand this to be a perfectly-timed opportunity—the chance to garner huge corpuses are possible only in the mid of an extended bull-run backed by a liquidity set-up.

• From a demand’ side perspective, the only rational explanation that seems to give can be found in the renewed business interests of many distributors. Addition of international stocks into folios as well as the need for diversification amidst correction-of-fears, can be a factor triggering the inflow into mutual funds.

While this innovation might actually be good for the industry, highlighting an increasing trend towards diversification and globalized investment, but at the end of the day the question remains is this wave driven by a structural change in demand or by all the wrong reasons?

❮

❯