Madhuchanda Dey

Moneycontrol Research

With GDP growth for the June 2019 quarter falling to a six-year low of 5 percent, it was imperative that the government would respond and “do something”. The finance minister has, albeit belatedly, responded to the situation. On Friday, just before the GDP numbers were announced, she held a press conference to propose the merger of several state-owned banks.

The criterion for the mergers was principally based on the commonality of the core banking platforms of the banks. Ten public sector banks have been combined under four new merged entities.

The first group consists of three banks operating under the Finacle technology platform – Punjab National Bank (PNB), Oriental Bank of Commerce (OBC) and United Bank – to create the second-largest bank in the public sector. Of these, PNB has a precarious capital position, OBC has just come out of the RBI’s Prompt and Corrective Action (PCA) framework and United Bank is still under PCA.

The second group is to be created by the merger of Canara Bank and Syndicate Bank, operating on the iFlex core banking platform and it will be the fourth-largest public sector bank. Both are present in the South and have relatively better financials and there will be synergies arising out of the merger.

The third group, also operating on the Finacle core banking platform, will be the fifth-largest public bank after the merger and involves Union Bank and Andhra Bank , along with Corporation Bank that has just come out of the PCA framework.

The last group involves two banks operating on the core banking platform BaNCS to create the seventh-largest public sector bank. The banks are Indian Bank, one of the better performing South-based banks and Allahabad Bank, a bank present mainly in the East that has just come out of the PCA framework.

One straightforward rationale of this exercise is to ensure better use of the capital that the government has promised to infuse (Rs 70,000 crore) that is expected to nurture them to health, enable them to comply with the RBI- stipulated capital adequacy norms and encourage them to start lending. Rather than sprinkling scare resources among multiple entities, the idea is to capitalise fewer but stronger entities so that they in turn can start lending.

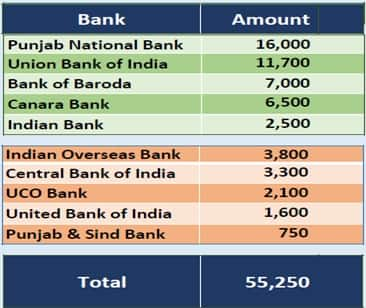

Tentatively, the recapitalisation is likely as follows (Rs crore):

Source: Government of India

But the more relevant question is, while technically a recapitalisation will strengthen their capital position, will it make a difference on the ground?

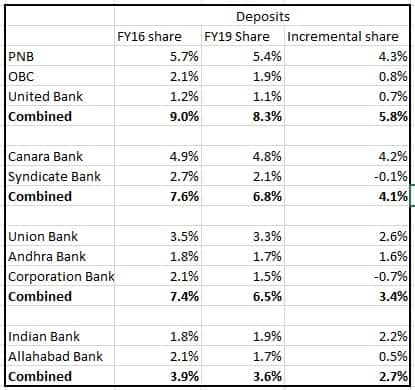

Let us look at the performance of these 10 banks on the credit and deposits front in the past three years and their market share in incremental business.

Source: Moneycontrol Research

As the chart shows, all the four newly-created entities have lost market share in deposits over the past three years. They have been losing market share in incremental deposits as well. Private banks have been agile enough to garner this share which has been lost by these state-owned banks.

Source: Moneycontrol Research

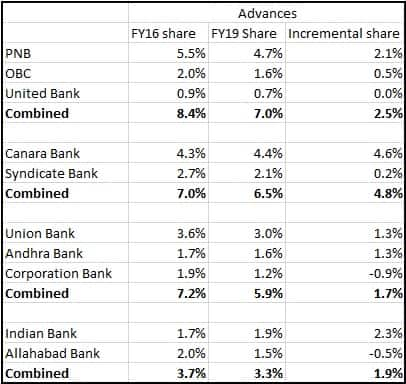

In the credit market, the picture is even more dismal for these 10 public banks. Their aggregate market share in credit has fallen from 26 percent to 23 percent in the past three years and their incremental market share is only 10 percent.

So, it is naïve to assume that they will recoup their business overnight as a result of the merger or the recapitalisation exercise.

Moreover, the formalities and complexities of merging such a diverse bunch of institutions, each with its own culture and processes, will consume the energies of the senior management. So, not much hope should be pinned on any improvements in the near term.

Governance reforms have also been announced, with permission to appoint risk officers at market-linked remuneration, the idea being to strengthen risk management practices in these banks.

While the consolidation of the state-owned banking sector is a long-term objective, it’s important to realise that the merged banks will continue to suffer from many of the same drawbacks that afflict the public lenders at present.

As for ensuring higher credit growth, it’s worth keeping in mind that lower credit growth is a consequence of the slowdown and not its cause.

For more research articles, visit our Moneycontrol Research page

Discover the latest business news, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!