In our 7th May report, we had highlighted the emergence of deep value in most of the auto stocks. The Auto sector has since been among the best performing sectors (outperformance of ~18.6pp over the Nifty in Q2CY20YTD). This is attributed to the kick-start of the recovery process post the lifting of the lockdown.

We are witnessing quick recovery in Tractors, followed by 2Ws and PVs, but CVs is yet to see any recovery. With incremental inputs, we have lowered our volume and EPS estimates for FY21/FY22. We prefer stocks that offer higher visibility in terms of demand recovery, a better competitive positioning, scope for margin surprises, and a strong balance sheet. MM and EIM are our top large-caps picks. Among the mid-caps, we prefer MSS.

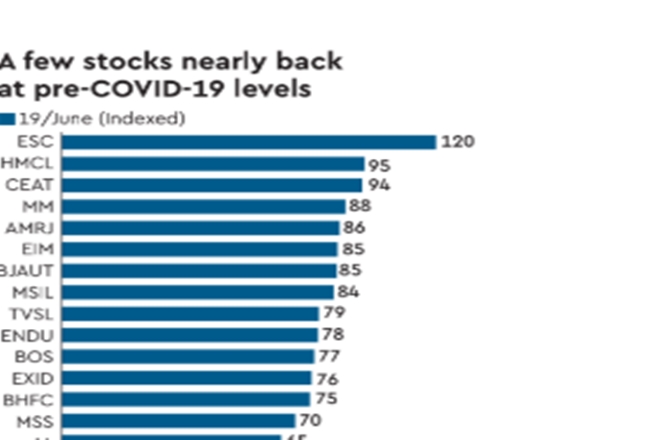

Sharp swing– from major underperformance to big outperformance

The Auto sector had reported sharp underperformance (43% decline and ~11.6ppunderperformance v/s the Nifty over Feb–Mar’20) since the COVID-19 outbreak (30thJan’20). However, since the gradual lifting of the lockdown (from 4th May), we have seen a sharp swing in the auto stocks. Top-performing stocks during this period were MM (+83% returns), MSS (+68%),ESC (+64%), and BHFC (+63%), while the worst-performing were EXID (+15%) and BOS (+19%). Effectively, auto stock valuations have normalised to ‘growth’ stocks from ‘deep value’.

What changed?

The outperformance has been driven by the slow restart of automotive operations in India. By mid-June, demand had recovered to 60–100% of pre-COVID-19 levels across segments. We have also moderated our volume estimates for FY21 across segments as additional inputs suggest a weaker 1HFY21 v/s our earlier estimates due to higher-than-anticipated supply-side constraints. We now expect more back-ended recovery; the segment is likely to surpass FY20 volumes only in FY23, except in Tractors. As a result, we have lowered our FY22 EPS estimates (v/s the 7th May report’s estimates) by 7–10% on average, with the highest cut for companies such as TTMT (-161%), EIM (-10%), MSIL (-7%), and TVSL (-8.5%) due to volume cuts.

Valuation and view

The COVID-19 pandemic has not only put the brakes on initial signs of recovery seen in 2Ws/PVs, but has also brought in uncertainty. This potentially deepens the impact of the BS6-related price increase on FY21 demand. Valuations are reflecting for recovery from 2HFY21, leaving limited margin for safety for any negative surprises.