Highlights:-

- Hot summers in Q1 will aid revenue growth

- Long-term prospects of the AC industry remain promising

- Our top picks are Amber Enterprises and Blue Star

--------------------------------------------------

FY19 has been a forgettable year for ACMs (air conditioner manufacturers). Weak summer conditions led to an inventory build-up across trade channels during the course of the year. To clear the same, the AC makers were forced to offer steep discounts and extend working capital cycles, especially in winter months (Q3 and Q4).

In spite of prevalence of winter conditions till the end of Q4 FY19 in most parts of the country, ACMs have been able to clear old stocks gradually, implying that business is back on track. We are optimistic about the growth prospects in this space. The factors are:-

- The penetration of ACs is very low in India, which indicates huge growth headroom

- Climatic conditions are tropical for most part of the year in most regions

- The government's emphasis on expanding electrification coverage

- Higher disposable incomes in hands of buyers

We prefer Amber Enterprises and Blue Star.

Outlook for Q1 FY20

Q1 FY19 turned out to be unusually weak for ACMs. This was on account of heavy thunderstorms in most parts of northern India during the quarter, which resulted in cooler temperatures and dampened demand for ACs. On an average, northern states constitute nearly 30-40 percent of the top line of ACMs. Consequently, the profits of ACMs dropped substantially since sales were heavily impacted.

In contrast, in Q1 FY20, summers have been harsh and also went on till the end of June -- almost across the entire nation. Therefore, on a low base quarter of last year, a visible improvement in revenue will be seen this time around. From a sequential perspective (i.e. compared to Q4 FY19), Q1 will be noticeably better as the benefit of seasonality kicks in -- Q4 is primarily a winter quarter whereas mercury levels start soaring in Q1.

Though year-on-year revenue growth is likely to be healthy, there is a possibility that it could be lower than expected. Here’s why:-

- Liquidity constraints continue to persist in the NBFC space, which may inhibit consumer financing

- From a macroeconomic perspective, the consumption sentiment remains subdued

Operating margin would be influenced by the following factors:-

- Volume growth in terms of AC sales

- Product mix (the contribution of inverter ACs to total revenue in particular)

- Cost controls

- Impact of raw material prices (due to movements in commodity prices and exchange rates)

Valuation – An overview

Which stocks should you consider?

Amber Enterprises is an ODM (original design manufacturer) cum OEM (original equipment manufacturer) player that manufactures RACs (room air conditioners) and components thereof. Client additions, impetus towards higher RAC volumes and foray into HVAC (heating, ventilation and air conditioning) projects should help Amber bolster its top line.

Operational efficiencies, product mix shift towards inverter RACs and benefits of inorganic growth strategies previously undertaken should enable margin accretion.

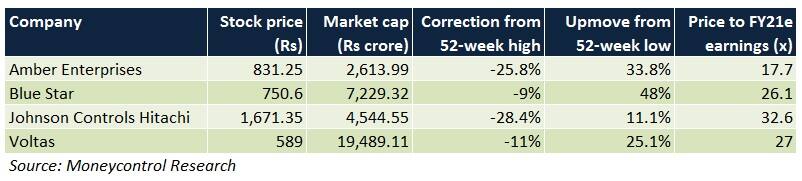

Amber is valued at 17.7 times its FY21 projected earnings. During the course of the past year, the stock, more often than not, has been trading in a range-bound manner, that is typically at Rs 800-850. We don't foresee a major downside from this point onwards. Therefore, this midcap should not be ignored.

(Also read - High mercury levels in Q1 FY20 will work in favour of this AC manufacturer)

For Blue Star, improving profitability in the electro-mechanical projects segment has been attributable to better project selection in India, focus on high-margin products and a positive outlook in its international markets.

In the unitary cooling products segment, market share gains in ACs, periodic product launches, an uptick in commercial refrigeration orders and brand-building investments for non-AC products should augur well.

In the professional electronics segment, the company is primarily banking on increased automation in manufacturing processes and data security systems to sustain demand momentum.

The stock, valued at 26.1 times its FY21 estimated earnings, has corrected quite a bit in the past one month. While it remains a fairly expensive pick, the moats of the business are convincing enough to merit the attention of new investors.

(Also read - Blue Star Q4 review: A good all-round performance)

Johnson Controls Hitachi aims to increase its market share in the HVAC (heating, ventilation and air conditioning) industry in a bid to achieve 15 percent revenue CAGR during the next 3 years. The management plans to enhance its reach in the tier 2/3 cities, south Indian markets and international geographies.

Growing contribution of high-margin chillers to overall revenue and local procurement of inputs should help derive operating leverage.

After correcting sharply in the past three months, the stock still remains pretty expensive (32.6 times its FY21 projected earnings). We advise accumulation on dips. However, trading volumes of this scrip tend to be very low at the exchanges.

Voltas’ electro-mechanical projects segment has been growing steadily on the back of government-funded urban infrastructure projects. In the Middle-East, Qatar-based operations are being normalised and opportunities are being explored in Bahrain.

In the engineering products and services segment, while textile machinery sales in India will go through a rough patch, demand for mining equipment in Mozambique is robust.

In the unitary products segment, the management intends to increase the AC manufacturing capacity to meet demand in southern and western India. Introduction of new models of inverter ACs and commercial refrigerators will also be on the agenda.

Under the 'Voltas Beko' brand, refrigerators, washing machines and microwaves will be promoted through advertisements and dealer incentives. This may dent margins of the unitary products segment -- roughly 50 percent of the yearly top line -- till the brand is well recognised. Consequently, we don’t foresee the stock re-rating significantly in the near future as it has been valued at 27 times its FY21 estimated earnings.

(Also read - Voltas Q4: Cooling products disappoint yet again)

For more research articles, visit our Moneycontrol Research page

Disclaimer: Moneycontrol Research analysts do not hold positions in the companies discussed here

Discover the latest business news, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!