Highlights:

- Mixed set of earnings from Crompton Consumer

- Electrical consumer durables grew nearly 10 percent

- Lighting division surprises positively on the margins front- Reasonably valued at 31 times FY20 estimated earnings

-------------------------------------------------

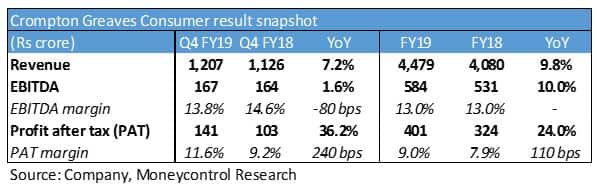

Consumer durable company Crompton Greaves Consumer Electricals (CGCE) saw a mixed financial performance in the final March quarter of FY19. While top line growth was steady, operating performance was subdued as margins were adversely impacted by commodity prices and increase in operating expenditures.

Key result highlights

- Revenue for the quarter increased by 7 percent year-on-year (YoY) to Rs 1,207 crore. However, earnings before interest, tax, depreciation and amortisation (EBITDA) came in nearly flat as the margins turned softer at 13.8 percent (vs 14.6 percent in Q4 FY18). Higher other income and reversal of tax payments aided the profit after tax, which increased 36 percent YoY.

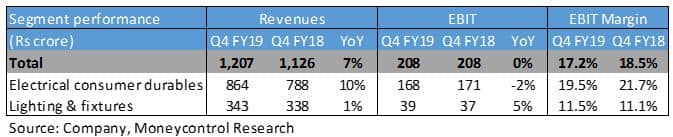

- Electrical consumer durables drove the overall top line growth. Higher contribution from premium fans, air coolers and pumps aided the quarterly revenues. Crest Mini (economy water pumps) continue to gain strong market traction both from the agricultural and domestic segments. Overall growth in the category was stronger in southern markets and the region witnessed double-digit growth. Segmental EBIT margins came under pressure due to higher commodity prices.

- The lighting and fixtures segment ended the year on a positive note as the margins witnessed a sharp recovery in January-March. However, lower contribution from the EESL business adversely impacted top line. The underlying performance was stronger as the segment volumes (ex-EESL) were higher by 25 percent and 11 percent in value terms. Price erosion in the LED business had adversely impacted the margins in the past 2-3 quarters. However, moderation in price decline in B2C (business to consumer) category, along with cost and design optimisation measures, helped the company post 11.5 percent margin in Q4 (vs 8.8 percent in Q3 and 6.6 percent in Q2).

- LEDs remain the key revenue driver for the lighting and fixtures business and now contributes around 85 percent to the segment’s top line. Going forward, the management plans to have a sharper focus on the B2B (business to business) segment and has invested in both people (key accounts manager) and technology (adoption of salesforce) to drive sales.

- The company aims to drive profitability through new innovative products (such as anti-bacterial bulbs) and rationalisation of the cost structure. Also, it's working to broaden its distribution footprint and looking to enter new product categories through the inorganic route.

Outlook and Recommendation

- The consumer durable market is set for a major push, given the low penetration levels of electronics. The growth is being fuelled by some recent trends like the electrification programmes and the rising income levels of consumers across urban and rural markets. The rapid growth in demand is attracting competition from multiple corners. Entry of newer players (Jaguar Lighting and Voltas Beko) along with the portfolio expansion by the existing players (LED Lighting by Indiabulls, Geysers by Cera) has crowded the market.

- From a business perspective, Crompton has a strong market positioning and remains well positioned to capture the demand in the market despite a hyper competitive market dynamics.

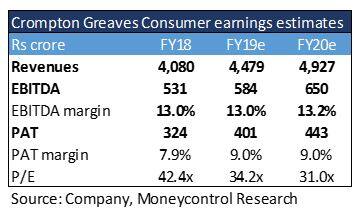

- From a valuation standpoint, Crompton (CMP: Rs 219 and market cap: Rs 13,743 crore) trades at a FY20 price earnings multiple of 31 times, which appears reasonable, considering its earnings visibility. The company enjoys a market leadership position in certain products (fans) and is focusing on product innovation, diversification and premiumisation to gain market share across other product segments. We, therefore, advise long-term investors to make use of any dips in the stock price to gradually build positions in Crompton Greaves Consumer Electricals.

Read: A shining star from the midcap cement pack

For more research articles, visit our Moneycontrol Research page

Disclaimer: Moneycontrol Research analysts do not hold positions in the companies discussed here

Discover the latest business news, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!