The September quarter performance of India’s banks has been one of the strongest in recent times. The industry has seen a sharp reduction in bad assets and a smart recovery in loan growth, which have contributed to a jump in the bottom line.

Stress, both legacy and fresh, has reduced for most lenders and loan demand is looking up from corporates and households. Balance-sheet heft has been a deciding factor as big lenders have outshone their smaller peers in performance.

Here is a look at the five key trends from the September quarter results:

1 Big goes better

Size matters when it comes to riding a crisis or even good times that follow. The September quarter performance of India’s banking sector shows this amply. The top three lenders—State Bank of India, HDFC Bank and ICICI Bank—are the stars of the recovery story.

All of them reported faster loan growth than the industry’s 16 percent. Together, they accounted for a quarter of the reduction in listed banks’ bad loan pile (HDFC Bank reported a marginal increase in bad loans, though). On the aggregate level, gross bad loans shrunk by Rs 50,000 crore year on year (YoY) for 30 listed banks that have released quarterly earnings, a Moneycontrol analysis shows.

No wonder then the top three lenders feature as the choice pick for most brokerages.

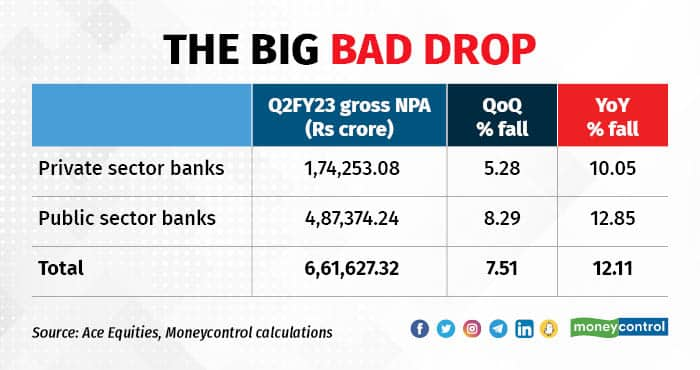

Public sector wins in asset quality

Public sector lenders reported the biggest fall in bad loan stock on a YoY basis. Gross bad loan stock of the 12 listed public sector lenders fell 15.8 percent for the September quarter, while that of listed private sector lenders fell by a smaller 13.2 percent.

Within public sector banks, lenders which had one of the worst bouts of bad loans showed the sharpest decline. Central Bank of India and Punjab & Sind Bank reported a near 30 percent reduction.

Bank of Baroda and Bank of Maharashtra reported more than a 20 percent fall. The decline in toxic loans was partly due to the upgrades and recoveries but write-offs played a big role as well.

Despite the reduction, most PSBs still have bad loans in excess of 5 percent of their loan book. Private sector banks’ gross bad loan ratio has ranged 4-5 percent with the exception of Bandhan Bank and South Indian Bank.

Profitability boost limited

While the bottom line of banks saw a 29 percent increase YoY at the aggregate level, not all lenders were fortunate enough to show a net profit boost.

Public sector banks witnessed a 44 percent jump in profits while private sector lenders showed 19 percent. Of the 18 listed private sector banks, four lenders showed a YoY decline in profits owing to either a hit on non-interest income or an increase in provisions.

Among public sector banks, three lenders showed a decline in profits. A handful of lenders increased provisions despite a fall in bad loans in order to shore up their provision coverage ratio. Anticipating stress in restructured loans was also one reason for increasing provisions.

Margins fatten, almost

Another high point of the September quarter earnings was the net interest margin. Margins swelled for most lenders as loan rates were hiked during the quarter.

The commentary from most bank managements on margins is mixed, though. While margins could remain stable or even expand a bit more in the coming quarters, the rate hike cycle will soon catch up with deposits.

Lenders have already begun hiking deposit rates and this will progressively increase the cost of funds for banks. Analysts believe that margins would come under pressure in FY24 and even earlier perhaps.

Watch out for stress

It may be counter-intuitive to worry about stressed assets when all lenders are reporting strong improvement. Granted, bad loan ratios have dropped for lenders but on a sequential basis, some lenders have shown an increase in fresh slippages.

HDFC Bank, IDFC First Bank and South Indian Bank reported a sequential increase in their bad loan pile. Other mid-sized banks have shown stress largely from small business loans and microfinance loans.

For all its stellar improvement in asset quality, SBI saw its recoveries and upgrades reduce sharply on a sequential basis.

Domestic inflation and global economic slowdown are two factors that could upset banks’ asset quality good luck trail. The jury is still out on stressed assets.

Discover the latest business news, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!