Breaking down ITC's first-ever analyst meet

Shares of ITC went up by 5% as soon as it was announced that its management would make presentations about the diversified business and take on analysts' questions head-on. Speculations of the widely discussed de-merger spread like fire as this was the first of its kind interaction with its investors who had high hopes with the tobacco-centered company.

However, after the meeting on Dec. 14, shares of the company came back to the levels where they have been trading for ages. So today, we try to decode what happened in ITC's first-ever analyst meet and what lies ahead for Sanjiv Puri in the challenging circumstances.

Expectations: As mentioned, speculations were on high that ITC is likely to unveil a new roadmap for the company, fulfilling an often-repeated investor dream of the non-tobacco segments like Infotech, Hotels being demerged and listed into separate entities.

Outcome: To the investors' surprise, the presentation did not even acknowledge such a future roadmap. Still, in response to analyst questions, CEO Sanjiv Puri did say they were open to the idea. However, it is important to note that the management has made such comments in the past as well

While this was ITC's first analyst meeting, the company had made similar presentations earlier centered around the themes of sustainability and investments in business diversification.

Key takeaways from the meeting:

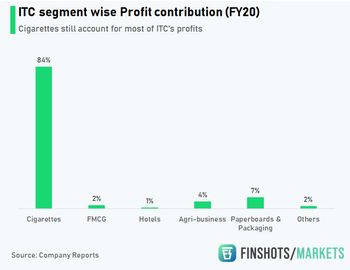

• ITC claimed its cigarettes business has the best segment profitability and margins worldwide. A sustained level of profits despite facing an adverse policy and taxation environment has helped the company to strengthen its proposition in focusing on the tobacco biz. Not to forget company draws 80% of its revenues from its cigarette business.

• Then came the slide on future corporate strategy that made it very clear as to what's on the cards. The management discussed 'structural interventions to drive margin expansion & capital productivity.' While this might sound heavy, it signalled nothing more than their intention towards internal business restructuring, like the decision to exit the apparel retailing business and other non-profitable segments but not the financial restructuring the investors were craving and attended for.

• Even in hotels, it has reiterated its stance on the 'asset-right' strategy, which might disappoint the investors. As per the available data, ITC owns 110+ properties in 75+ locations under different brand names. For a long time, investors have been demanding interventions towards an asset-light strategy as the hotel business has been prone to risks and adversely affected by the industry's cyclicality. However, the hopes went into smoke recently when ITC announced two premium megaprojects-Storii and Momentos, bolstering its aggressive stand on the hotel business

• It is also clear that the company is positively looking towards acquisitions to add valued brands to its portfolio of products. ITC has been quite successful in turning around brands such as Savlon (acquired from Johnson and Johnson in 2015), Sunrise foods (2020), Nimyle (2018), etc. However, it is not very clear whether this will have a sizeable impact in improving contribution from the FMCG business.

What lies ahead?

Ultimately, the question being asked is what will drive the ITC share from its current levels? It does not matter how much we ignore it, but the answer lies in the cigarette business. Mr. Puri has been quite vocal about how the Sustained period of high taxes affected tax revenue collections which is their biggest concern as of now. And it's that time of the year again when all eyes are on the budget. It won't be incorrect to state that because of the nature of business, ITC gives the bureaucrats more power in deciding ITC's fate than its own management exposing its vulnerabilities to the outside world.

❮

❯