Impact of RBI’s move to introduce PCA on NBFCs

The Reserve Bank of India’s (RBI) move to bring Non-Banking Financial Companies (NBFCs) under its Prompt Corrective Action (PCA) framework will have a minimal impact and will largely be neutral for the sector as the companies covered under the scope are already complying with the norms.

The move is to make NBFCs more vigilant going forward and to avoid a repeat of a DHFL or an IL&FS like episode. This will ensure NBFCs stay more alert and not come under the scanner of RBI after the default has happened.

Despite this, the shares of NBFCs including #HDFC, #BAJAJFINSV, #CHOLAHLDNG, #MnMFIN, #MUTHOOTFIN and Shriram Transport Finance slipped between 1-3 percent intra-day on the NSE on Wednesday.

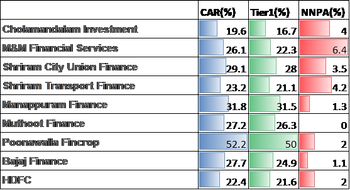

The RBI on Tuesday introduced a PCA framework for large NBFCs, putting restrictions on para-banks whenever vital financial metrics dip below the prescribed threshold. The main parameters would be capital-to-risk weighted assets ratio (CRAR), Tier 1 ratio and net non-performing assets (NPAs) including non-performing investments.

According to the new guidelines, PCA will be triggered if CRAR falls below 300 bps below the regulatory requirement or Tier 1 capital declines to 200 bps below the regulatory requirement or net NPAs go beyond 6 percent. This move will act as a deterrent and discipline the sector.

The framework will come into effect on October 1, 2022, on the basis of the financial position on or after March 31. It will be applicable for all deposit-taking NBFCs. Those not taking deposits and with an asset size of less than Rs. 1000 crore, government owned NBFCs and housing finance companies are exempt from this framework.

Currently, M&M Financial Services is the only listed NBFC that has net NPA in the excess of 6 percent but it can conveniently bring it down to less than 6 percent by the end of FY22. Similarly, Tata Motors Finance has a net NPA ratio of 7.34 percent as of Q2FY22. Another large company with a net NPA ratio of over 6 percent is Hero FinCorp.

The regulations will be a mixed bag for the sector as it will benefit larger NBFCs. The restrictions, if imposed on any smaller player, will reduce the competition for bigger NFCs. Hence, highly capitalized NBFCs, with as good NPA check mechanism in place, need not worry, while smaller financiers will now have to be careful from now on.

The return ratios, such as return on equity or return on investment, may decline going ahead if NBFCs decide to raise buffer capital as a precautionary measure.

PCA being extended to NBFCs may prove to be a good decision for the long term as it will encourage good practices and is also expected to improve governance. Investors must be careful and must include parameters like NPAs and capital adequacy ratios in their screening criteria and not compromise with any breach in these parameters. Asset quality of any NBFC must be carefully monitored before making investment in it.