#TANLA is in the same accumulation zone of Feb - Oct 2021 and is in downtrend with the falling relative strength. The price is reflecting the state of IT index.

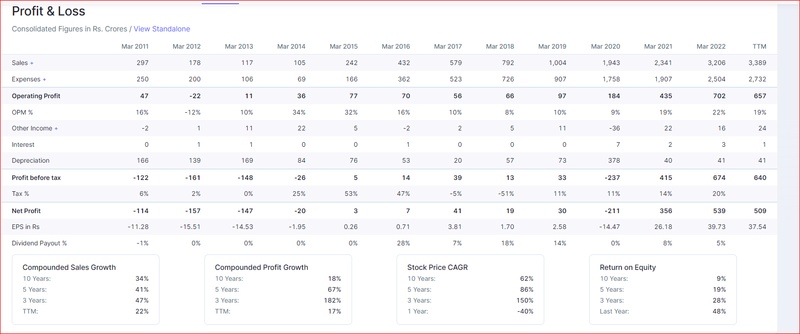

Fundamentally, the company looks good with great ROCE and ROE numbers. The sales growth of last 5 years is 40% with very low to negligible debt to equity ratio.

The operating margin is in good range of 19 to 22% for last couple of years. The price to booking is little high, about 7 times.

The company, as far as the numbers are concerned looks good for investment. If anyone is holding this from lower levels, can average at this level. For fresh position, I believe that price will go lower from here, once it stabilises at the base of the zone marked around 585-600.

From trading point of view, wait for the price to close above 200 Day EMA and relative strength to improve.

I have checked some of the recent concalls, the customer base looks good. However, not sure what is the challenge because of which the price is getting beaten down, must be either competition or recessionary pressure in FY23 impacting the margin.

Please share your views in the comment section.

❮

❯